If you’re self-employed in Canada, you’ve probably felt the sting of CPP contribution time. While your salaried friends have their contributions quietly split with their employer, you’re sitting there writing a cheque for the whole thing yourself. It feels unfair. But before you write off CPP as a raw deal, it’s worth understanding exactly what you’re paying, why, and — most importantly — what’s coming back to you in retirement.

This is the full breakdown.

Why Self-Employed Canadians Pay Double

Let’s start with the basics. When someone is employed, CPP contributions are split 50/50 between the worker and their employer. As a self-employed person, you are both the employee and the employer — so you pay both halves out of your own pocket.

That means while a salaried employee contributes 5.95% of their pensionable earnings, self-employed Canadians contribute at a combined rate of 11.9%. Every dollar you earn from your business is working twice as hard to fund your future pension.

The 2026 Numbers in Plain English

Let’s put real numbers to this. The maximum CPP contribution for employees and employers in 2026 is $4,230.45 each. If you are self-employed, your maximum contribution is $8,460.90.

Your contributions are calculated on your net business income — meaning after you’ve deducted your business expenses. You do not contribute on investment earnings or other types of income. So if you grossed $100,000 but had $25,000 in legitimate business expenses, you’d only contribute on the remaining $75,000 (minus the $3,500 basic exemption).

For higher earners, there’s now a second tier called CPP2 — and it applies to you too.

| Benefit | Salaried Worker | Self-Employed |

| CPP Retirement | Yes | Yes |

| CPP Disability | Yes | Yes |

| Survivor Benefits | Yes | Yes |

| Pays Both Halves? | No | Yes |

What Is CPP2 and How Does It Affect Self-Employed Canadians?

CPP2 is a relatively new addition to Canada’s pension system, introduced in 2024. It was designed to extend CPP coverage to higher earners who previously had no pension contributions on income above the first ceiling.

If you’re self-employed, you pay both the employee and employer portions of CPP2 — 8% on income that falls between $74,600 and $85,000. You report and pay this when you file your T1 return.

The self-employed CPP2 maximum contribution in 2026 is $832, up from $792 in 2025.

When you add CPP and CPP2 together, the maximum combined contribution for a self-employed individual in 2026 is approximately $9,292. That’s a significant annual cost — but the silver lining is that contributing to CPP2 translates into higher monthly pension payments down the road. The more you contribute now on higher earnings, the higher your CPP payments will be once you retire.

The Tax Deduction Most Self-Employed Canadians Miss

Here’s where many self-employed Canadians leave money on the table. You don’t have to absorb the full cost of paying double with no relief.

You can claim a deduction for the employer-equivalent portion of your CPP contributions on your personal tax return, effectively reducing the after-tax cost. In other words, the “employer half” of what you pay is treated as a deductible business expense — similar to how an actual employer deducts their share.

This doesn’t eliminate the cost entirely, but it does bring the real after-tax burden down considerably. Depending on your tax bracket, this deduction can save you thousands of dollars each year. If you’re not already claiming this, talk to your accountant — it should be standard practice on every self-employed tax return.

So What Do You Actually Get Back?

This is the question that really matters. After years of paying double, what does retirement actually look like?

The good news: CPP contributions on self-employment income earn exactly the same retirement, disability, and survivor benefits as employment income contributions. You are not penalized or shortchanged on the benefit side just because you work for yourself.

Your CPP retirement pension is based on how long you contributed and how much you earned during your working years. The maximum monthly CPP retirement pension for individuals starting at age 65 in January 2026 is $1,507.65, with the average monthly payment for new recipients sitting at $925.35.

Beyond retirement income, your CPP contributions also cover you for:

CPP Disability benefits — if you become unable to work due to a severe and prolonged disability

Survivor’s pension — a monthly benefit for your spouse or common-law partner if you pass away

Children’s benefits — payments for dependent children of deceased or disabled contributors

Death benefit — a one-time lump sum payment to your estate

For self-employed Canadians who don’t have access to employer group benefits, workplace disability insurance, or a company pension plan, these CPP protections are arguably even more valuable than they are for salaried employees.

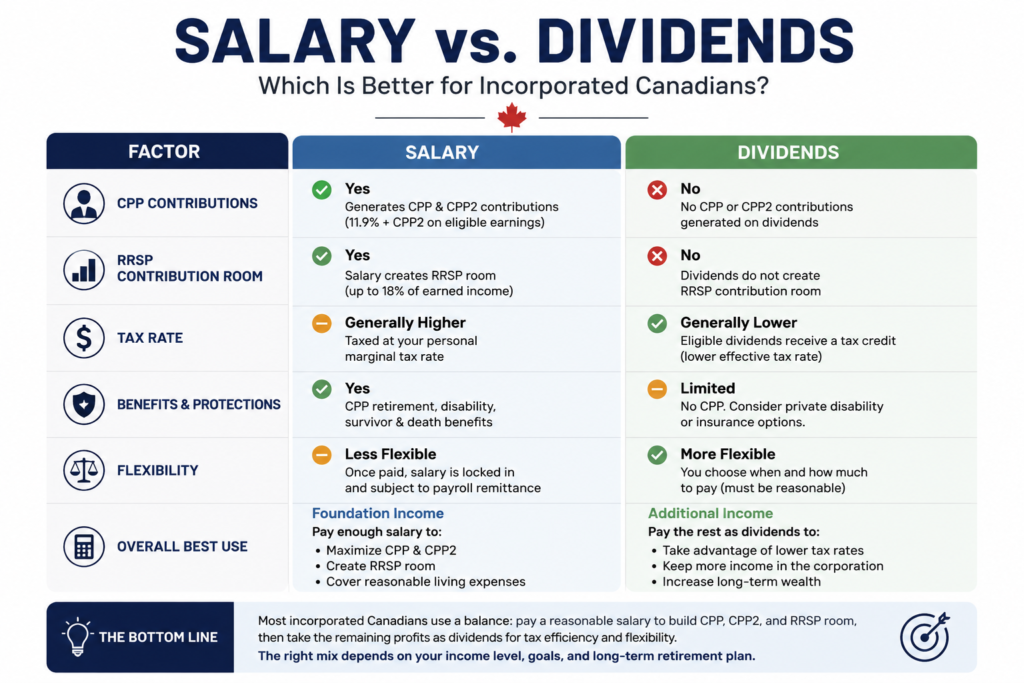

The Incorporated Business Owner Question: Salary vs. Dividends

If you operate through a corporation, you face a decision that salaried self-employed Canadians don’t: should you pay yourself a salary, dividends, or a mix of both? This is where CPP planning gets more strategic.

Many business owners look at the 11.9% CPP contribution rate and decide to pay themselves entirely in dividends, which sidesteps CPP contributions altogether. On the surface, this looks like a smart tax move. But the trade-offs run deeper than they appear.

The case for salary: CPP creates a guaranteed income stream in retirement. One of the most consistent things retired business owners report is that they want a portion of their income to just arrive in their account every month, predictably, regardless of what markets are doing. Salary also generates RRSP contribution room. Dividends don’t generate RRSP contribution room — only salary does. Your annual RRSP limit is 18% of your prior year’s earned income, up to the 2026 maximum of $32,490. If you pay yourself entirely in dividends and accumulate no RRSP room, you lose that flexibility permanently — you can’t go back and reclaim unused room from years you paid yourself dividends.

The case for dividends: In 2026, the cost of paying a high salary has slightly increased due to CPP2. For earnings between $74,600 and $85,000, there is now a second tier of contributions at 8% for the self-employed. This makes high salaries more expensive than in previous years, which may tilt the math further in favour of dividends for high-earning owners who don’t prioritize CPP benefits.

The smart middle ground: Many incorporated owners take a mix — a minimum salary to generate some CPP contributions and RRSP room, then dividends for the rest. A common approach is to draw $50,000 to $74,600 in salary to maximize CPP contributions, then take additional income as dividends. For many incorporated Canadians, a thoughtful blend of salary and dividends produces better lifetime results than committing to only one method. With retirement costs rising in 2026 and longevity increasing, those long-term outcomes matter more than squeezing out a small tax saving in a single year.

There’s no universal right answer here — the best strategy depends on your income level, province, retirement goals, and how much you value the predictability of guaranteed CPP income versus flexibility. This is exactly the kind of decision worth reviewing with a CPA who works with small business owners.

Practical Tips for Managing CPP as a Self-Employed Canadian

Budget for it throughout the year. Unlike salaried employees who have CPP deducted automatically from every paycheque, self-employed Canadians pay their CPP as part of their annual tax filing. Getting hit with an $8,000+ bill in April is painful — set aside a percentage of every invoice payment throughout the year so it doesn’t catch you off guard.

Build it into your rates. Your CPP contributions are a real cost of doing business. If you haven’t factored them into how you price your services, you’re effectively undercharging. Think of the employer half of your CPP the way a corporation thinks of payroll costs.

Claim the employer deduction every year. This is non-negotiable. The employer-equivalent half of your CPP contribution is deductible from income. Make sure your tax software or accountant is claiming this properly every single year.

Check your CPP Statement of Contributions. Log into your My Service Canada Account and review your Statement of Contributions annually. This shows exactly how much you’ve contributed over your working life and gives you a projection of your future monthly pension. It’s one of the most useful retirement planning tools available — and most Canadians never look at it.

Don’t assume CPP replaces a retirement plan. Even at the maximum, $1,507.65 per month is not a retirement income on its own. Treat CPP as one piece of the puzzle alongside your RRSP, TFSA, and any other savings vehicles.

The Bottom Line

Yes, paying double CPP contributions is one of the real costs of self-employment in Canada — and CPP2 has added another layer on top. But self-employed Canadians get back exactly the same benefits as anyone else: a guaranteed, inflation-indexed monthly pension for life, plus disability and survivor protections that are especially valuable when you don’t have an employer benefits package to fall back on.

The key is to plan around it — price your services to account for it, claim every deduction you’re entitled to, and if you’re incorporated, work with an accountant to find the right salary-dividend mix for your situation.

Your future self — the one collecting a reliable pension cheque every month in retirement — will thank you for it

As always thanks for reading,

Greg

- CPP for Self-Employed Canadians in 2026: The Full Picture on Paying Double — and What You Actually Get Back

- Another Oil Shock Is Coming — Are Canadian Retirees Ready?”

- The New Retirement Threat: How the Iran War Could Hit Your CPP, OAS and Investments

- Draining your RRSP before OAS Kicks In

- Why More Canadians May Have to Work Longer Than Planned

Disclaimer

The information provided on this blog is for general informational and educational purposes only. It is not intended to be, and should not be taken as, financial, legal, or tax advice. While we make every effort to ensure the information is accurate and up to date, government benefit amounts, contribution rates, and eligibility rules can change. Always verify current figures directly with Service Canada or the Canada Revenue Agency.

We strongly recommend speaking with a qualified financial advisor, accountant, or legal professional before making any decisions about your CPP, OAS, or retirement planning. Every individual’s situation is unique, and professional guidance is the best way to ensure you’re making the right choices for your circumstances.

This blog is not affiliated with, endorsed by, or connected to the Government of Canada, Service Canada, or the Canada Revenue Agency.