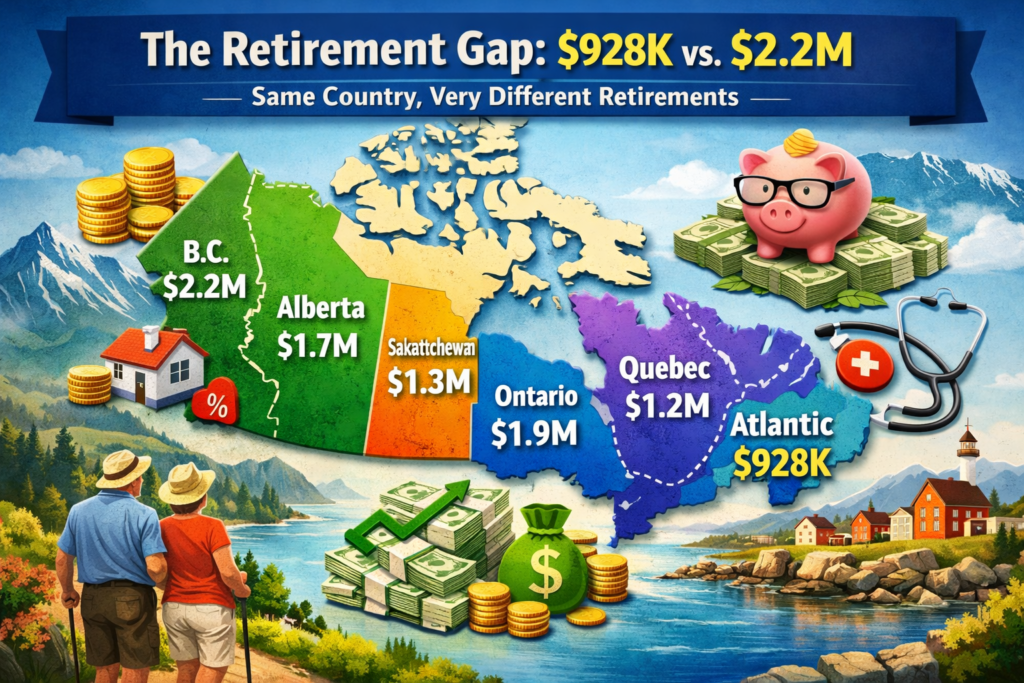

Ask someone in Vancouver what they need to retire and ask someone in Halifax the same question — you’ll get very different answers. That’s not just a matter of opinion. According to BMO’s Annual Retirement Survey, it’s a nearly $1.3 million difference.

B.C. residents set the national high at $2.2 million. Atlantic Canadians come in at around $928,000. And every province in between tells its own story about housing, taxes, and the cost of everyday life.

Nationally, the average target is $1.7 million — up from $1.54 million last year. And where you live explains almost everything about that gap.

Here’s what’s actually driving those numbers.

Why B.C. Retirement Targets Are So High

The biggest driver is simple: cost of living.

Housing prices in British Columbia — particularly in cities like Vancouver and Victoria — are among the highest in Canada. Even for retirees who own their homes, property taxes, insurance, maintenance, and everyday expenses remain elevated.

Groceries also tend to cost more here. Because much of B.C.’s population is concentrated in the Lower Mainland and on Vancouver Island, food distribution and retail pricing often reflect higher transportation and retail costs. Anyone who shops regularly knows the bill adds up quickly.

Then there’s lifestyle. Many people move to B.C. for the quality of life — oceans, mountains, mild winters, and outdoor recreation. But that lifestyle comes with a price tag.

When daily expenses are higher, retirement savings targets naturally climb with them.

Alberta: Lower Taxes, Lower Target

In Alberta, the retirement estimate drops to about $1.7 million. One of the biggest reasons is tax policy.

Alberta has no provincial sales tax, which immediately reduces the cost of everyday purchases. Income taxes can also be somewhat lower depending on income level.

Housing, while rising in recent years, is still generally more affordable than in major B.C. or Ontario markets. Cities like Calgary and Edmonton offer relatively strong infrastructure and healthcare access without the same housing pressures.

Lower ongoing expenses mean retirees may need less capital to sustain their lifestyle.

Saskatchewan and Manitoba: Quietly Affordable

Both Saskatchewan and Manitoba come in at roughly $1.3 million for retirement expectations.

Housing affordability is one of the biggest advantages. In many communities across these provinces, homes can cost a fraction of what they do in Vancouver or Toronto.

Food and basic living costs are also generally lower. Agriculture plays a major role in the local economies, which can help keep grocery prices relatively stable.

Healthcare access is another often-overlooked factor. While rural areas may face some shortages, smaller populations can sometimes mean shorter wait times and less strain on the system compared with large urban centres.

For retirees who value space, quieter communities, and lower expenses, these provinces can stretch retirement dollars much further.

Quebec: Lower Living Costs, Unique Tax Structure

Quebec’s estimated retirement target sits around $1.2 million.

Housing prices, especially outside Montreal, remain relatively affordable compared with other large Canadian cities. Day-to-day living costs can also be lower in many regions.

However, Quebec does have higher provincial income taxes than most provinces. That said, the province also offers more extensive social programs, childcare support, and certain healthcare benefits, which can offset some financial pressures for residents.

For retirees who plan carefully around taxes, Quebec can still provide a relatively affordable retirement.

Atlantic Canada: The Lowest Retirement Target

The Atlantic provinces — including Nova Scotia, New Brunswick, Prince Edward Island, and Newfoundland and Labrador — report the lowest retirement estimate at around $928,000.

Housing remains significantly cheaper than in most of the country, especially outside Halifax. Many retirees from Ontario and B.C. have been relocating east to take advantage of lower property prices and a slower pace of life.

Food costs can sometimes be higher in smaller communities due to transportation logistics, but overall living expenses are still generally lower.

Healthcare access can vary by region, but many retirees appreciate the strong sense of community and quality of life.

The Bigger Concern: Many Canadians Aren’t Saving Enough

While retirement targets are rising, savings habits haven’t necessarily kept pace.

The survey found:

∙ 28% of Canadians save less than 5% of their income

∙ 38% save between 5% and 10%

∙ 21% save more than 10%

Looking at monthly savings:

∙ 10% save less than $100

∙ 23% save $100–$499

∙ 10% save $500–$999

∙ 12% save more than $1,000

Those numbers highlight a growing concern: many Canadians worry they won’t reach their retirement goals. Rising housing costs, inflation, and economic uncertainty make long-term planning more challenging than it used to be.

Retirement Is Changing

Another interesting shift is how people think about retirement itself.

About 14% of Canadians say they don’t plan to retire at all. For many, that doesn’t mean working forever in a traditional job. Instead, retirement might look like part-time work, freelancing, consulting, or passion projects and small businesses.

In other words, retirement is becoming less about stopping work entirely and more about having flexibility and financial independence.

The Real Takeaway

The amount you need for retirement isn’t just about investment returns or savings rates. It’s heavily influenced by where you choose to live.

A million dollars might stretch comfortably in parts of Atlantic Canada or the Prairies, while the same amount could feel tight in Vancouver or Toronto.

That’s why retirement planning shouldn’t focus on a single national number. It needs to reflect lifestyle choices, location, and personal priorities.

For some people, that may mean saving more. For others, it may mean simply choosing a place where their money goes further. 🌎

Check out other blog posts here

As always, thanks for reading,

Greg

Disclaimer: This article is for informational and educational purposes only and should not be considered financial, investment, or tax advice. Every individual’s financial situation is different. Readers should consult with a qualified financial professional before making investment or retirement planning decisions.