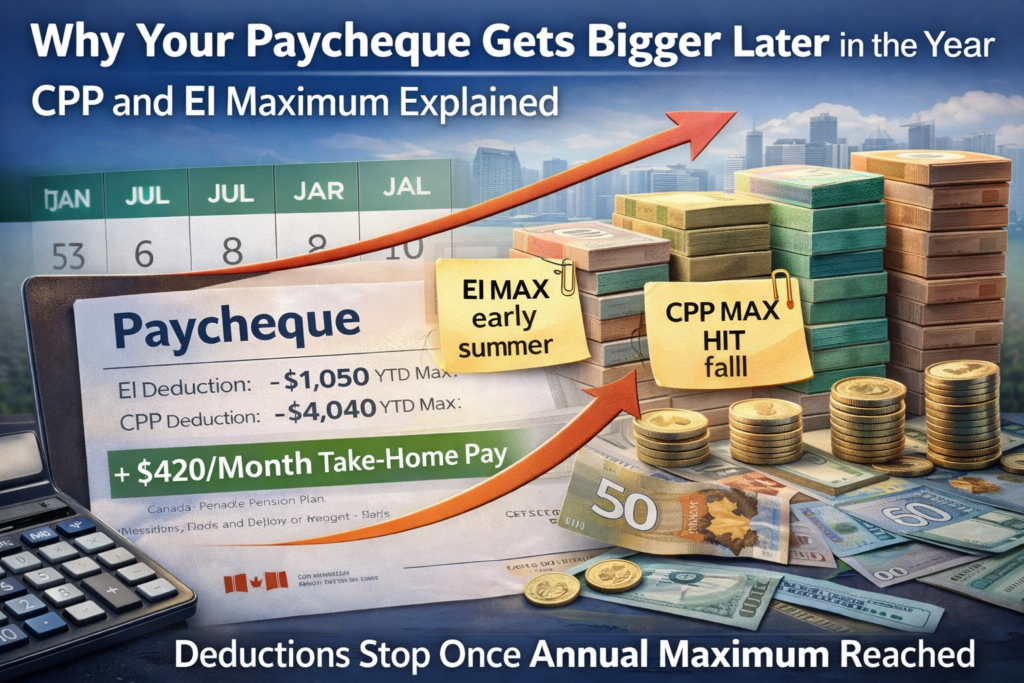

Many Canadians notice something strange happens to their pay later in the year.

Suddenly, their take-home pay increases — even though their salary hasn’t changed.

No raise.

No bonus.

Just more money in the bank.

Here’s why.

The Real Reason Your Net Pay Increases

In Canada, two payroll deductions have annual maximum limits:

- Canada Pension Plan (CPP)

- Employment Insurance (EI)

Once you reach the yearly contribution limit, those deductions stop for the rest of the calendar year.

When the deductions stop, your take-home pay goes up.

CPP Contributions (2026)

CPP is deducted to fund your future retirement pension.

2026 estimates:

- Contribution rate: 5.95%

- First $3,500 of income is exempt

- Maximum pensionable earnings: about $71,300

Maximum employee CPP contribution:

~$4,040 per year

Higher earners may also pay a small additional CPP (CPP2), bringing the total close to $4,400–$4,500.

Your employer contributes the same amount.

EI Contributions (2026)

Employment Insurance covers benefits such as job loss, parental leave, and sickness benefits.

2026 estimates:

- Contribution rate: 1.66%

- Maximum insurable earnings: about $63,200

Maximum employee EI contribution:

~$1,050 per year

Once you reach that amount, EI deductions stop.

When Do Deductions Stop?

For many full-time workers:

- EI usually stops first (late summer)

- CPP stops later (fall or early winter)

After that point, your paycheque can increase by:

$100 to $300+ per month, depending on income.

That’s often why people notice their pay suddenly looks higher toward the end of the year.

Example

If you earn $80,000 per year:

- EI stops once you’ve contributed about $1,050

- CPP stops once you reach roughly $4,040+

- After both maximums are reached, you keep the extra amount that would normally be deducted

Same salary.

Higher net pay.

Does This Affect Your Retirement?

Yes — and this is important.

CPP contributions determine your future retirement benefit.

If you consistently earn near the maximum and contribute fully each year, you’re building toward a higher CPP pension.

For 2026, the maximum CPP retirement benefit at age 65 is roughly:

$1,400–$1,500 per month

(if you contributed at or near the maximum for most of your career).

What About OAS?

Old Age Security (OAS) is different.

- You do not pay into OAS

- It is funded through general tax revenue

- There are no payroll deductions for OAS

A Planning Tip

When your CPP and EI deductions stop:

Instead of letting the extra cash disappear into spending, consider:

- Increasing RRSP contributions

- Adding to your TFSA

- Paying down debt

- Building your retirement income plan

That extra money is an opportunity.

The Big Picture

CPP and EI maximums aren’t a bonus — they’re simply the point where you’ve fully contributed for the year.

But understanding how payroll deductions work helps you:

- Plan your cash flow

- Avoid confusion when pay changes

- Build stronger long-term retirement income

Final Thought

Retirement security isn’t built with big moves.

It’s built by understanding the small ones.

As always — invest in time, not just money.

How CPP Contributions Today Affect Your Retirement Income

CPP isn’t just another payroll deduction — it’s building your future retirement pension.

Every year you contribute based on your earnings, that year counts toward your CPP calculation.

Your retirement benefit depends on:

- How many years you contributed

- How much you earned each year

- Whether you contributed near the maximum

- The age you start CPP (60–70)

Why the Annual Maximum Matters

If your income is at or above the CPP maximum earnings level, you’re earning a full contribution year.

Over time, consistent maximum contributions can qualify you for:

Close to the maximum CPP benefit, which in 2026 is roughly:

- ~$1,400–$1,500 per month at age 65

- Higher if you delay to age 70

But here’s the part many people don’t realize:

If you earn below the maximum for many years, your CPP will be lower — sometimes significantly.

Missing Contributions Can Reduce Your Pension

Your CPP retirement amount is based on your average lifetime contributions.

Lower benefits can result from:

- Part-time work

- Career breaks

- Self-employment with low reported income

- Working outside Canada

- Years with little or no earnings

CPP does allow some low-earning years to be dropped, but long periods of low contributions will still reduce your future income.

Why Higher Earners Reach the Maximum Faster

If your salary is high, you reach the annual CPP maximum earlier in the year.

That doesn’t reduce your future pension.

It simply means:

You’ve already made your full contribution for that year.

From a retirement perspective, that year counts as a full-value CPP year.

What This Means for Retirement Planning

Think of CPP as a foundation:

- Maximum contributions for 35–40 years → near maximum pension

- Lower or inconsistent contributions → smaller lifetime income

- Delaying CPP to age 70 → increases payments by up to 42%

For many Canadians, CPP will provide:

$12,000–$18,000 per year

That’s helpful — but not enough on its own.

That’s why the extra take-home pay you see after CPP and EI stop each year is an opportunity to:

- Increase RRSP or TFSA savings

- Pay down debt

- Build additional retirement income sources

The Big Retirement Lesson

CPP deductions may feel like a cost today.

But each year you contribute is buying:

- Guaranteed lifetime income

- Inflation protection

- Government-backed security

And that kind of income becomes more valuable the longer you live.

CPP & EI Maximum 2026

Why Your Paycheque Gets Bigger Later in the Year

2026 Contribution Limits (Employee)

CPP

- Contribution rate: 5.95%

- Maximum pensionable earnings: $68,500

- Basic exemption: $3,500

- Maximum employee CPP: ~$3,867

CPP2 (Second Tier – higher earners)

- Additional rate: 4%

- Applies to earnings between $68,500 – $73,200

- Maximum CPP2: ~$188

Total Maximum CPP (2026): ~$4,055

EI

- Contribution rate: 1.66%

- Maximum insurable earnings: $63,200

- Maximum employee EI: ~$1,049

What This Means

Total Maximum Deductions (CPP + EI): ~ $5,100

Once you reach these limits:

CPP and EI stop — your take-home pay increases for the rest of the year

Source: CRA annual contribution limits (2026)

Every CPP contribution is a small payment toward future financial independence.

As always — invest in time, not just money.

Greg