By Greg March 2026

If you have an RRSP in Canada, there is an important deadline you cannot ignore. By the end of the year you turn 71, your RRSP must be converted into a Registered Retirement Income Fund (RRIF) or another income option such as an annuity.

Once your RRSP becomes a RRIF, the government requires you to withdraw a minimum amount every year. These withdrawals are fully taxable and the required percentage increases as you age.

Understanding how RRIF minimum withdrawals work is critical for retirement planning because large withdrawals can push your income higher and potentially trigger issues like the OAS clawback.

Below we explain the rules and show the current RRIF minimum withdrawal rates by age.

What Is a RRIF Minimum Withdrawal?

A RRIF minimum withdrawal is the minimum amount the Canada Revenue Agency requires you to withdraw from your RRIF each year.

Key rules include:

- You must convert your RRSP to a RRIF by December 31 of the year you turn 71.

- Withdrawals begin the following year.

- The minimum withdrawal is based on your age (or your spouse’s age if elected).

- All RRIF withdrawals are taxable as income.

There is no maximum withdrawal, but taking more than the minimum can increase your tax bill and affect government benefits.

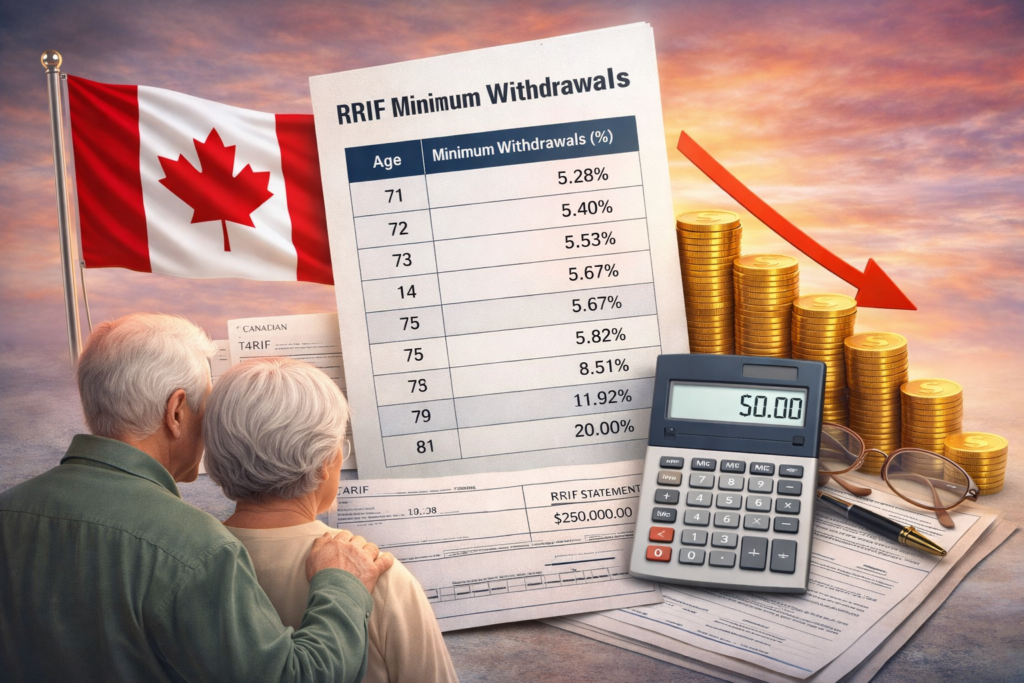

RRIF Minimum Withdrawal Rates by Age (2026)

The minimum withdrawal percentage increases gradually as you get older.

| Age | Minimum Withdrawal % |

| 71 | 5.28% |

| 72 | 5.40% |

| 73 | 5.53% |

| 74 | 5.67% |

| 75 | 5.82% |

| 76 | 5.98% |

| 77 | 6.17% |

| 78 | 6.36% |

| 79 | 6.58% |

| 80 | 6.82% |

| 81 | 7.08% |

| 82 | 7.38% |

| 83 | 7.71% |

| 84 | 8.08% |

| 85 | 8.51% |

| 90 | 11.92% |

| 95+ | 20.00% |

For example:

If you are 72 years old with a $500,000 RRIF, your minimum withdrawal would be:

$500,000 × 5.40% = $27,000

This amount must be withdrawn during the year and reported as taxable income.

Use this calculator to estimate the minimum RRIF withdrawal required by CRA based on your age and account balance.

The minimum RRIF withdrawal is calculated using the CRA formula:

RRIF balance divided by 90-your age

Example , if you are 72 with RRIF balance of $500000, the minimum withdrawal is about $27,778

Using Your Spouse’s Age

A common planning strategy is to base your RRIF withdrawals on your younger spouse’s age.

This lowers the minimum withdrawal percentage and can help:

- Reduce taxes

- Delay higher withdrawals

- Limit the risk of triggering the Old Age Security (OAS) clawback

This election must be made when the RRIF is first established.

How RRIF Withdrawals Affect Taxes

RRIF withdrawals are treated as ordinary taxable income.

They are added to your income along with:

- CPP payments

- OAS pension

- Employment income

- Investment income

Large RRIF withdrawals can push your income into higher tax brackets or cause part of your OAS pension to be clawed back if your income exceeds the annual threshold.

Because of this, many retirees try to manage withdrawals carefully.

Strategies to Reduce RRIF Tax Impact

With proper planning, many retirees can reduce the tax impact of RRIF withdrawals.

Common strategies include:

1. Pension Income Splitting

RRIF income can often be split with a spouse, helping reduce the overall tax burden.

2. Early RRIF Withdrawals

Some retirees withdraw funds earlier in retirement when their tax bracket is lower.

3. TFSA Withdrawals

Withdrawals from a Tax-Free Savings Account do not count as taxable income, making them useful for managing total income.

4. Coordinating CPP and OAS

Deciding when to start CPP and OAS can affect how RRIF withdrawals impact your tax situation.

Why RRIF Planning Matters

Many retirees focus on saving for retirement but underestimate how withdrawal rules affect taxes later in life.

Without a plan, mandatory RRIF withdrawals can:

- Increase your tax bracket

- Trigger the OAS clawback

- Reduce government benefits

- Create unnecessary tax bills

Careful income planning can help keep more of your retirement income working for you.

Final Thoughts

RRIF minimum withdrawal rules are designed to ensure retirement savings are gradually withdrawn and taxed. While the percentages start relatively small, they rise steadily as you age.

Understanding the withdrawal schedule and planning ahead can help you manage taxes, protect government benefits, and create a more predictable retirement income strategy.

If you are approaching age 71 or already have a RRIF, reviewing your withdrawal strategy early can make a significant difference over the long term.

As always thanks for reading ,

Greg

Planning your retirement income involves many moving pieces.

Browse our other articles on CPP benefits, OAS rules, RRSP strategies, RRIF withdrawals, and retirement planning in Canada.

© 2026 www.canadaretirementincome.ca ·Retirement Income Strategies for Canadians For informational purposes only · Not financial advice

Jusst do your research before choosing an agent to see what

promotions and bonuses they offer.